Economic wrap-up for May 2026

Stats SA published 25 statistical releases in May, with many providing a preliminary snapshot of economic performance in the first quarter (January–March).

Business indicators largely upbeat

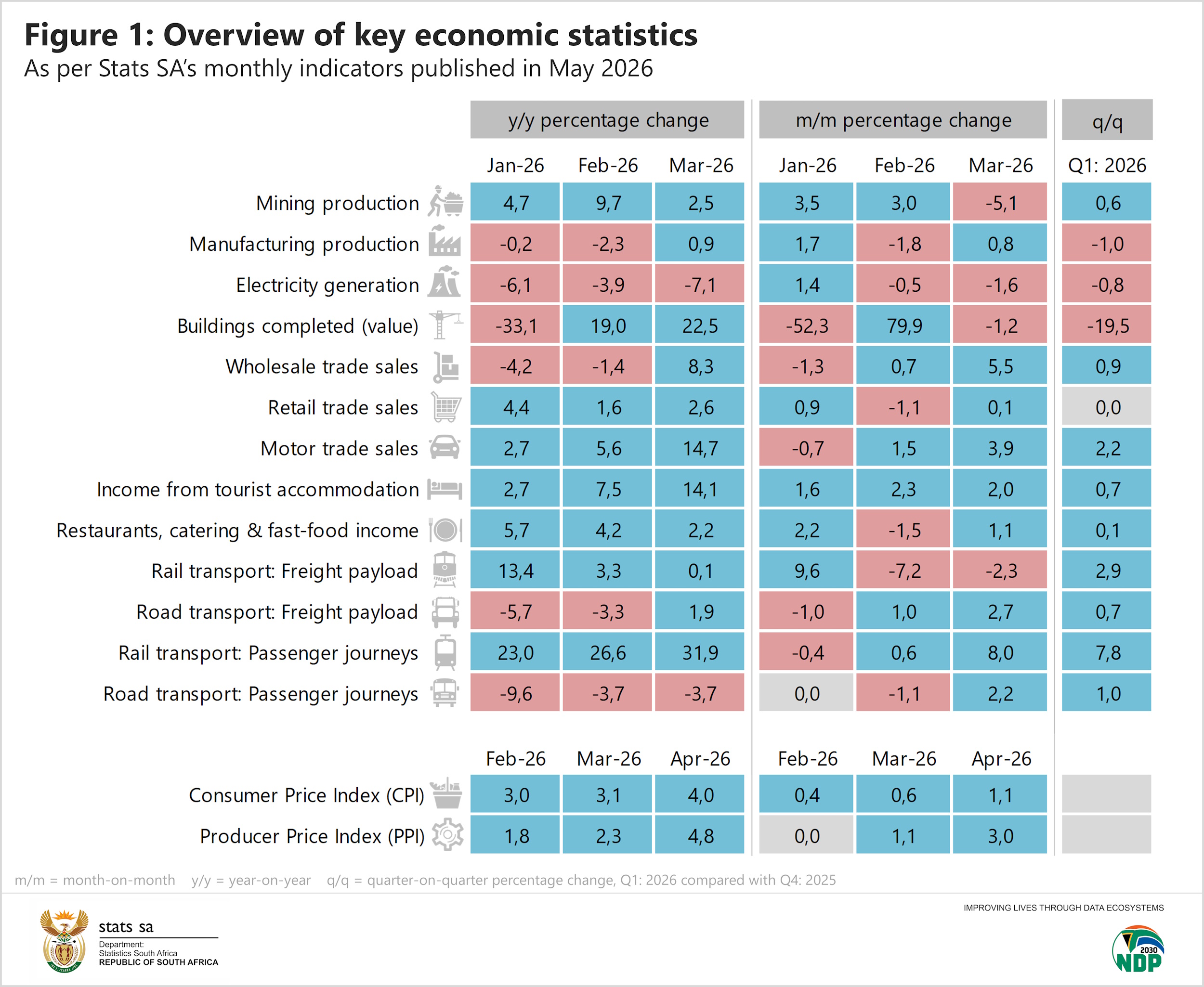

The first quarter of 2026 was mainly positive, with stronger results from mining; wholesale trade sales; motor trade sales; tourist accommodation; restaurants, catering & fast-food; and rail & road transport (see Figure 1 below).

Mining production expanded by 0,6%. Platinum group metals made the largest positive impact, growing by 8,5% and contributing 2,3 percentage points to overall growth. The mining industry also produced more diamonds, gold and chromium ore. However, there was a decline in the production of manganese ore, coal, iron ore, nickel and copper.

Motor trade sales remained positive, growing for a fourth consecutive quarter. The 2,2% rise in the first quarter was mainly supported by stronger vehicle and fuel sales. Used vehicle sales recorded the highest growth rate, rising by 4,8%. The new vehicle market extended its gains, registering a sixth consecutive quarter of growth.

On the downside, manufacturing, electricity generation, and construction (buildings completed as reported by large municipalities) were weaker in the first quarter.

Manufacturing experienced a second straight decline, weakening by 1,0%. Five of the ten manufacturing divisions reported lower production levels, with the petroleum, chemical products, rubber & plastic products division the most significant negative contributor. Other divisions that were weaker include wood, paper, printing & publishing; iron & steel, non-ferrous metals & machinery; communication & professional equipment; and food & beverages. The first quarter marked the sixth consecutive decline for the iron & steel, non-ferrous metals & machinery sectors.

South African electricity generation edged lower by 0,8%. This followed decreases in the third quarter (-1,8%) and the fourth quarter (-3,2%) of 2025.

After enjoying eight straight quarters of upward momentum, retail trade sales stalled, registering zero growth in the first quarter. Four of the seven retail groups were stronger, with retailers in household furniture & appliances recording the highest growth rate (+1,8%). The positive influence of the four retail groups was offset by declines in food & beverages; general dealers; and hardware, paint & glass.

Unemployment rate rises

The mostly positive outlook in the first quarter was dampened by the latest labour force data. The official unemployment rate rose to 32,7%, the highest reading in three quarters. The labour force shed an estimated 345 000 jobs, with the biggest losses recorded in community & social services and construction. Five other industries also recorded job losses. Three industries recorded modest employment gains: agriculture; mining; and manufacturing.

The data also show that youth (aged 15–24) currently face the highest unemployment rate at 60,9%.

Fuel prices cast a shadow over inflation

The sharp fuel price increases in April drove up both consumer and producer inflation. The headline rate for the consumer price index (CPI) jumped from 3,1% in March to 4,0%, the highest print in 20 months. The monthly change was 1,1%, driven mainly by painful increases in diesel (+35,4%) and petrol (+15,2%).

Fuel price increases also affected prices at the factory gate, as measured by the producer price index (PPI). The annual PPI headline rate jumped to 4,8% in April from 2,3% in March, driven mainly by higher prices in the coke, petroleum, chemical, rubber & plastic products category. This is the highest print in two years. Petroleum-related products experienced record price increases, including petrol, diesel, fertilisers, petrochemicals & feedstock and bituminous mixtures.

Future statistical releases

Several key outputs are due for release in June. The next gross domestic product (GDP) estimates will provide a comprehensive overview of economic performance in the first quarter. The results will be published here on 9 June at 11:00.

Three statistical reports highlighting government data are also expected in the month. The first will cover national government finances for the 2024/25 fiscal year and the second municipal finances for the first quarter. The third will provide annual financial data for municipalities. All three reports will be published on 25 June.

For those interested in building statistics, Stats SA will release its 2025 set of data on building plans passed and buildings completed by the private sector (as reported by large municipalities) on 23 June.

Stats SA will reintroduce statistics of insolvencies in July 2026. The release will report the total number of individuals and partnerships placed under final sequestration. The statistics of insolvencies for June 2026 will be published on 21 July 2026.

Interested to know more? Keep up to date with our publication schedule. For a comprehensive list of products and releases, download our catalogue. For a regular update of indicators and infographics, visit our data story feed and download the latest edition of the Stats Biz newsletter.